The way we talk about banking technology has completely changed. For years, the goal was "digitalization," which meant putting modern screens on top of old systems. Today, that is not enough. In a market with intense competition and growing, complex risks, using old systems is not just inefficient; it is a major business risk. The failure of these rigid financial systems to adapt to new forms of data, customers, and threats is costing institutions a lot of money in lost market share and increased operational risk. A true digital lending transformation is no longer optional.

For Chief Risk Officers and Heads of Lending, the results are clear. Inefficient digital onboarding leads to high customer drop-off rates. The inability to accurately approve loans for new market segments, like gig economy workers, means losing valuable customers to faster FinTechs. This article provides a strategic analysis of the four major changes defining the new financial landscape. It also offers a clear framework for leading a successful digital lending transformation that turns technology from a risk into a competitive advantage.

The financial technology sector is experiencing a significant separation of the traditional risk management process. Four connected technological and strategic changes are driving this trend, creating an environment where only the most adaptable institutions will succeed.

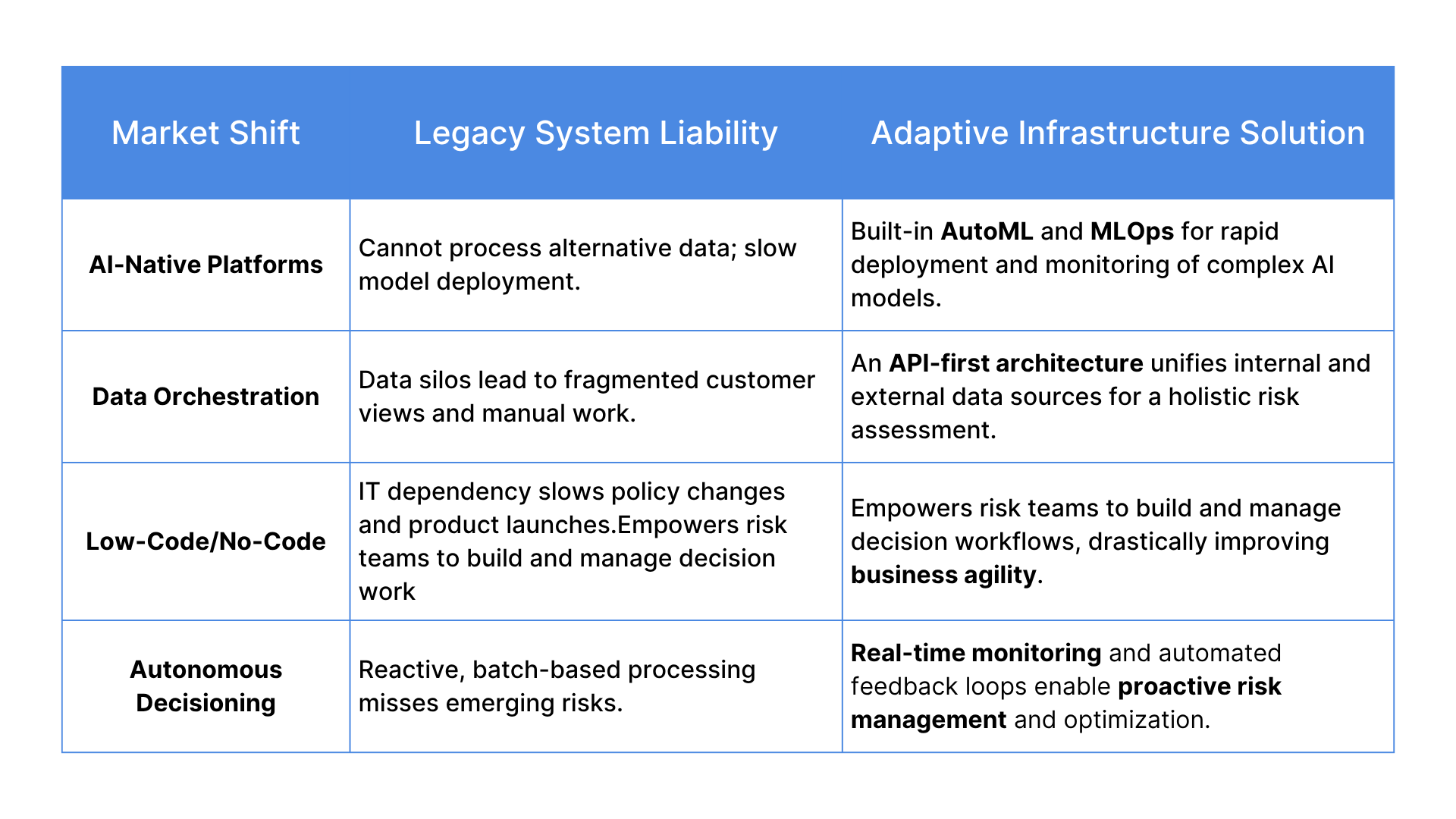

The market has moved from adding small AI features to using platforms that were built for artificial intelligence from the start. This is not just a trend. It is a response to two market needs: the need to analyze large, alternative data sets for more accurate loan decisions and the urgent requirement to fight more advanced, AI-powered fraud.

An AI-native platform is fundamentally designed for the complexities of machine learning. This means it can easily use and process different types of data, allow for fast model deployment, and provide strong tools for continuous monitoring and retraining of AI models.

Why Legacy Systems Fail: Traditional banking systems were built for a world with simple, structured data from credit bureaus. They are not flexible enough to handle the speed and variety of alternative data (like utility payments or mobile wallet usage) that modern AI credit scoring models need. Trying to add AI on top of this old foundation results in weak, slow, and poor-performing risk models.

A decision engine's value depends on the quality and accessibility of its data. Because of this, the ability to easily integrate, manage, and connect data from many sources is now a key area of competition. Modern platforms act as a central place for data intelligence. They use a single API to connect to dozens of sources, from credit bureaus and government databases to alternative data providers.

Why Legacy Systems Fail: The problem of data silos is a major weakness of old banking systems. When customer data, transaction history, and risk information are stored in separate, disconnected systems, it is impossible to get a complete view of the customer. This leads to incomplete risk assessments, missed sales opportunities, and a slow onboarding process.

A major trend in the market is giving more power to business users who are not technical experts. These are the credit risk managers, fraud analysts, and compliance officers who know the business best. A low-code decision engine gives these experts visual, drag-and-drop tools to design, deploy, and change complex decision workflows without writing any code.

This trend directly solves the delays within financial institutions, which often deal with IT departments that have too much work and not enough specialized technical staff.

Why Legacy Systems Fail: In an old system, even small changes to a credit policy can require a long and expensive IT project. This creates a damaging reliance on IT that stops new ideas. The business side cannot react quickly to changing market conditions or launch new credit products. This means losing the ability to move quickly compared to faster competitors who can change their strategies in hours, not months.

The next step in risk automation is moving from systems that help people make decisions to systems that manage risk by themselves. This involves advanced AI systems that can not only score an application but also automatically perform and coordinate complex related tasks with very little human help.

Why Legacy Systems Fail: Legacy systems are designed to react, not prevent. They are built for historical reporting, not real-time analysis and action. They do not have the real-time monitoring and feedback systems needed for autonomous decisioning. This leaves risk managers always looking at the past instead of preparing for the future.

These four changes point to one main problem: the failure of traditional, rigid systems to adapt. The solution is not to make small, separate improvements. It is to make a fundamental change to an Adaptive Decisioning Infrastructure, a platform that is flexible, works with all data, and is built on an AI-native core.

This modern approach treats risk decisioning as one dynamic business function, not a separate technical problem. Here is how it directly solves the challenges from the market changes:

For senior banking leaders, championing this shift from a legacy liability to an adaptive asset requires a strategic approach.

Step 1: Audit Your Decisioning Bottlenecks Begin by mapping your end-to-end lending lifecycle, from application to collection. Identify the key points of friction. Where do manual reviews create the biggest backlogs? How long does it take your IT team to implement a simple policy change? Quantifying these inefficiencies (e.g., "We spend 300 man-hours per month on manual income verification") is the first step to building a compelling business case.

Step 2: Build the Business Case Around Agility and ROI Frame the investment not as a cost center but as a revenue driver. Use tangible metrics to project the ROI, focusing on outcomes that matter to the C-suite:

Step 3: Prioritize a Unified, No-Code Platform To achieve true agility, you must break the cycle of IT dependency. Champion a platform with a no-code workflow builder that allows your credit and risk teams, the people who understand the business logic, to own the entire policy lifecycle. This ensures that your decisioning strategy is transparent, auditable, and can adapt at the speed of the market. The Synapse Konan platform is built on this principle, empowering business users to control decision logic from end to end.

Step 4: Embrace a Champion/Challenger Approach to Innovation A modern AI risk decisioning platform allows you to test new models and strategies safely in a production environment. Use champion/challenger frameworks to continuously compare the performance of your existing models (the "champion") against new ones (the "challengers"). This data-driven approach allows you to iterate, learn, and optimize your strategies, ensuring your models deliver continuous improvement and a measurable lift in portfolio performance.

The era of monolithic, inflexible banking technology is over. The digital lending transformation is not about incremental improvements; it's about fundamentally re-architecting how decisions are made. The four shifts: the rise of AI-native platforms, the necessity of data orchestration, the empowerment of business users, and the move towards autonomous decisioning, have created a new competitive reality.

Institutions that continue to rely on legacy systems are accepting a future of higher costs, increased risk, and shrinking market share. By embracing an Adaptive Decisioning Infrastructure, you empower your organization to not only survive these shifts but to leverage them as a powerful engine for growth, efficiency, and market leadership. The tools to make this transformation a reality exist today.

Is your institution ready to lead the change? See firsthand how an AI-native, no-code decisioning platform can solve your most pressing lending challenges.

Join leading financial institutions in leveraging AI to revolutionize your lending processes.